It’s TIME to ELEVATE your LIFE!

STARTING A CAREER IN INSURANCE. INSIGHTS YOU SHOULD KNOW.

Information anyone starting this career should know . . .

Truth builds Trust

If new agents had someone to give them some real advice starting out, how much would it help them? Perhaps they wouldn't have lost money and time trying their best to make a great living. Maybe they wouldn't be at the point of throwing in the towel forced back to a JOB they hate. How many good people are wondering "how have others been successful in this career?"

This page will hopefully help you have the insight that can help avoid being taken advantage. We want you to start from a winning position.

Situations to AVOID -vs- Starting from a WINNING Position

WASTED MONEY

Investing a LOT of money with a company that doesn't have skin in the game (do they REALLY have your interest at heart?)

There are companies that charge you for leads up-front with your own money before you can go to work. They buy their leads from vendors and then, mark them up and re-sell them to you making money off you. To us, that is nothing more than a way for them to make money off licensed agents whether those agents are successful or not.

How can you get leads without investing a ton of money?

Many people do not know there are companies that will provide leads, with ZERO money out-of-pocket.

How to get inventory the RIGHT way . . . ZERO money out of pocket. SERIOUSLY

Our agents are NOT required to spend any money out of their pocket, up-front to get leads. Write business, and the cost of the leads will come out of the production. AND, we will pay you half of your advance and use half to repay the lead balance.

Example:

You take $1,000 worth of leads

Your write 10 policies from those leads worth $10,000

Let's say the first policy is small and has an advance of $1,000. We do not take the full $1,000.

You get PAID $500, and $500 goes back toward your balance

Let's say policy 2 is the same amount and has a total advance of $1,000. You get PAID $500 and $500 clears your balance.

NOW, policy three is the same and has the same $1,000 advance. Your lead balance has been cleared and you then get the full $1,000!

In this scenario, you got PAID while clearing your lead balance and never paid a cent out of your pocket. THEN, once it was cleared, you got the full advance.

NON-OWNERSHIP

Being an employee for an insurance agent -vs- being the OWNER of your business. Are you working for someone else and making them rich while you get very little for your efforts?

When you get your license, you will be recruited by companies. Take a look around at how many insurance agencies are in strip malls around you. They hire people to come to work every day, and work for them helping customers. Let's say you do this and they tell you they will give you a "base pay" plus some commission for every policy you help them write.

You are an employee doing the work and helping that agent make the majority of the money.

If they are on a 100% contract (for every $1,000 of policy sold, they get $1,000), and they tell you they will pay you $100 as commission, you are doing the work and they are making the money. Congratulations, you're still someone's employee helping make them rich and you are not the boss. Whoever is signing your check, is on 100% commission and making the most money

Be the Owner of Your Business

When you are contracted directly with the insurance provider, you get rewarded for your work. You are an OWNER of your business! You worked very hard to get your license. You made a decision to stop working for crumbs while making others rich. Why would you then turn around and go right back to working for someone else?

Some people say, "I like the security of a guaranteed paycheck." That's fine. But look at who is signing that check. We suggest that every single person who owns a business (the person who signs the check) is 100% commission and makes more money.

Many newly licensed agents take positions working for other licensed agents because they simply do not know how to go about getting the same opportunity. They do not know those opportunities exist. They DO.

We proudly represent Lincoln Heritage (the largest final expense provider in the United States) and our agents are contracted directly with them. Our agents ARE true agents and their business is THEIR business.

FAKE UP-FRONT TRAINING EXPENSES

Paying for an expensive "training program" with an agency or insurance company to go through their "mentorship" program (paying to go to work)

There are companies that actually charge new hires to go through their "training programs". To us, this is absolutely rediculous. They require people to pay THEM directly to study for their licensing test, then pay to take the test, then pay to apply for their test with the state.

Let's be clear, you SHOULD have skin in the game. It's YOUR career. BUT, when they charge you to pay THEM to study, they are just trying to make money (sometimes a LOT more than the price for an online from-home, at-your-pace course), while requiring you to spend set me with them. They ALSO, then charge you to go through a "mentorship" program for weeks/months/years, before you actually start making a living.

Invest in your license, then get PAID!

The cost to prepare yourself to pass the test should be reasonable. The cost to take the test is a set price. The cost to apply for your state's license is set by the state. THAT'S ALL you should pay up front. PERIOD.

We get asked often if we cover the cost of getting your license. We will reimburse you for the cost of your license application once you are appointed with us and have written your first policy, with our company. If you get your license and decide to go with another provider, we do suggest you ask them to do the same.

We HIGHLY suggest you do NOT pay the company you are going to work for to train you for the test. Use a reputable online, or in-person company that specializes in this training. We suggest XCEL Testing Solutions, which is an online, work-at-your-pace course. They are the top provider for life, health and accident pre-licensing training.

Other pre-licensing courses can cost $200 and more . . .

We have had heard stories of agents spending a LOT more to go through a "mentorship" program costing them almost a $1,000 without ever making any money. We help you get licensed for less out of pocket.

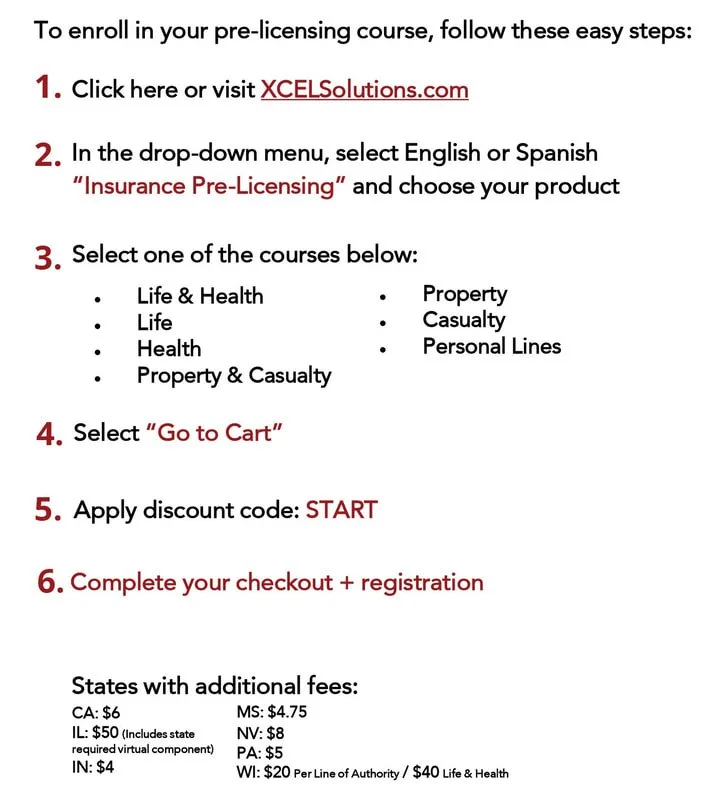

Instructions and Discount Code

We send a LOT of people to XCEL Testing Solutions, because we have seen the results. Because we send many people to them, they give our referals a discount code. If you found them on your own, they charge $199 for their course. That's STILL a very good deal. Because of the volume of new agents we send XCEL, they provide a discount code to save you $100. Use the code "START" and the course will only be $99.

You can visit their site: https://www.xcelsolutions.com/

Step 1: Select the course you need

Step 2: Select your state

Step 3: Click Continue

At check-out, enter code: START

This will give you a $100 discount!

(We have included more info at the bottom of this page)

Actual mentorship and REAL training

Then, you should be getting trained by a mentor who is actually DOING the business today. AND, preferably by someone who is willing to help YOU get paid while in training. Our process is, a manager will take you out, work with real clients and split the commissions on the policies that are written.

We also believe training is an ongoing process. Being part of a team of people, who do what you do, and are willing to share their experiences is invaluable. Find a company that is willing to tell you the good and bad. When you have a team that will share learning experiences, you gain knowledge faster and you ability to earn better and quicker becomes a win!

BAD OPPORTUNITY

How bad is the reputation of your insurance provider? Know their history. Are they going to be able to follow through on the promises made?

Do a little research. You have invested time and money into starting this career. Consider the reputation of the company you decide to represent. Do they ACTUALLY follow-through on their promises? Not only to your clients but to YOU?

Misleading BIG contracts (100% or higher), is it legit? We have heard stories of new agents being told that company has agents on a contrat of 150%. How many? What are the requirements? That particular company actually got a letter fom the Federal Trade Commission telling them basically to stop lying to new agents.

Is the insurance company reinsured? If they are, it basically means, if they had to pay all their claims and commissions, they don't have the money to do so. Is your commission safe?

Long-term benefits: Can the company you do business with pay your residuals? What are the requirement to actually KEEP your residuals? There are companies that make big promises of long-term, residual income, but then hide loopholes to get out of paying them. For example: You spend a career building up your residuals (retirement) income, then when you decide to retire, find out you only have 90 days to clear up any lead or chargeback debt. There are people who have lost their entire retirement because that was not enough time. What other loopholes are there?

Chargebacks: How does the company you work with handle charge-backs? Chargebacks are a part of the business. There are companies that will require you send them voided check to your bank account so they can go into your account and take money back OUT. Even if the money in your account wasn't money paid from that company (grandma gave you money for your birthday) for example. They will require access to take even that money as payment back on a chargeback.

WINNING OPPORTUNITY

Let's keep this simple. We represent a company that puts you in a winning opportunity . . .

REAL contract percentages that are clearly described. And, ability to increase your contract clearly outlined

Highest rating by the BBB

Nominated for the "Torch Award" the highest award for ethics from the BBB

Highest rating by AM Best for our kind of business

1 YEAR to clear any lead/chargeback debts so you can KEEP your residuals

We put $ IN your bank, not take it out

Chargebacks work like leads. They come out of production. You can simply produce away any debt instead of writing a check or having money come out of your bank that was given to you by grandma

WAITING FOR YOUR INCOME

Not getting paid in a timely manner. Not getting paid the AMOUNT or WHEN you were promised

If you are required to wait to get paid monthly, weekly or bi-weekly . . . why? Does that company not have enough money to pay you today? Are they sitting on your income making interest and not sharing it?

Why are you not being paid your commissions DAILY?

Get Paid Daily

There should be a simple relationship between good people who work and the company they represent. You do the work promised and they follow-through and pay you. TODAY

Our agents can get paid daily (Monday - Friday). Our pay schedule is simple. When you write a policy on our digital application and it's submitted and the first payment comes out, you get paid. We don't sit on your income for a month to make interest while you are trying to pay your bills. We are here to help you, not hurt your family.

COMPLICATED BUSINESS

Difficult underwriting processes to get the policies you submit actually approved. Doing work and only 50% ACTUALLY being approved. And a LOT of paperwork before and after the policy starts.

There are a LOT of types of insurance on the market. Many products require an agent to go sell the policy (juggle through a LOT of different types of confusing policies with their clients), then submitt lots of paperwork to the provider, then the company will send someone to the client's house the perform a physical (or require the client to go somewhere for a physical) then wait for the results to get back to the provider, then have an underwriting department review the results and look for a reason to approve or deny the policy.

Let's say that agent is on a 100% contract, but ONLY 50-60% of those policies are ACTUALLY approved. Is that agent really on a 100% contract? About half their work was for nothing.

THEN, that agent is also required to do a lot of paperwork when to file claims on policies, or do a lot of related paperwork for policies when changes are needed (service work).

Do you want to spend your days doing a bunch of paperwork?

Do you want to spend your days struggling to do complicated business?

KEEP IT SIMPLE AND PRODUCTIVE

Our agents spend their time helping clients and their families. Our application is ONE PAGE and SIMPLE. We understand that time is valuable. The easier we make our business, the more families our agents can help. We do everything we can to keep it SIMPLE so there is less wasted time. This also makes for happier agents.

Hopefully, this page has helped give you some direction and answered some questions about this career.

As promised, below is more information on a GREAT company that has great results preparing you for this opportunity.

Be sure you to use code; "START" when you check out to save some money.